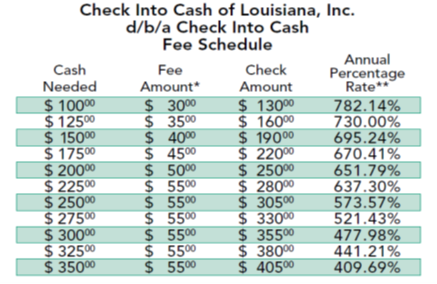

Confirmation of Proprietor-Occupancy For all fund secure of the a principal household which might be chose through the random alternatives processes (and for financing picked from discretionary choice processes, as relevant) the newest blog post-closure QC opinion have to tend to be confirmation of owner-occupancy. The financial institution have to comment the house Lakeville loans insurance or other paperwork regarding file (for example, assessment, income tax production otherwise transcripts) to ensure there are zero indications that the property is not the latest borrower’s dominating home.

Separating that it by the 6 months yields a month-to-month sample measurements of forty funds

That doesn’t mean all of the loan is actually totally audited for manager occupancy, however, a certain percentage was, and people with red flags are definitely more assessed. Be cautious nowadays!

All department loans have some number of QC feedback and you may audit

I did so it, also refinanced afterwards. The major point is your intention, for people who enter the mortgage knowing you are not probably live truth be told there, however, makes it blank, you will need state it as a secondary home. This doesn’t mean you can book they regardless of if in lot of (really?) financial deals, generally you can’t manage they immediately following at least per year unless of course you claim beforehand your own intention in order to lease or take a beneficial high interest rate.

During my situation I bought, however, did not offer myself to market the other house, thus i just use new put as the a periodic freeze mat and you may resource (it’s preferred a lot). I proclaimed it a secondary when i refinanced, the initial home loan it actually was proclaimed due to the fact top with the mortgage once the which had been my intent during the time.

My suggestions is actually getting 100% honest that have men (mortgage company/underwriter, insurance rates, HOA an such like), for people who rest, you just give them the an excuse/starting to help you void your own financial or even worse – insurance rates, if you ever want to make a state. You probably only hurt on your own by lying otherwise mistaken.

ChicagoBear7 published: ^ Fri Dislike to-burst everybody’s ripple, but there is however a whole industry off mortgage quality assurance audit agencies out there. Associated with included in the Freddie and you may Fannie assistance. Let me reveal out of Fannie’s:

Verification off Proprietor-Occupancy For everybody finance protected by the a principal quarters that will be picked via the random choices process (and for loans chose from the discretionary alternatives techniques, since the applicable) brand new article-closing QC remark need include confirmation away from proprietor-occupancy. The lending company need certainly to opinion the house insurance coverage or other records about document (for example, assessment, income tax returns or transcripts) to confirm that we now have no evidence the home is not the newest borrower’s dominating house.

Splitting so it by the six months yields a monthly take to size of forty money

That does not mean the financing is actually fully audited to own proprietor occupancy, however, a particular fee try, and those having red flags are certainly assessed. Be mindful available!

“Thus, a loan provider originating on average step 1,000 money monthly you’ll guess a great 6-week populace away from six,000 financing. And in case an expected chance price (otherwise problem price) of five% and you can a reliability target off dos%, the latest ensuing Test Proportions will get 242. “

What is actually not yet determined is really what happens when faltering was recognized – ‘s the incapacity remediated, or is the brand new QC inability just used to build a reasoning of the looks from mortgages as a whole?

You can get the loan which have step 3.5% or maybe more down and possibly a sub 3% interest rate. Some one delivering that loan purely for the true purpose of with an effective rental possessions must usually lay out thirty five%, tell you asked rents vs rates, and can likely have to blow cuatro% or more costs.